When you notice water pooling near your basement walls or cracks forming in your concrete slab, your first thought might be: homeowners insurance will cover this, right? Not so fast. Foundation leaks are one of the most confusing and frustrating claims homeowners face-and too many people assume their policy will pick up the tab, only to get denied when they file. The truth? Most standard policies won’t cover foundation leaks unless they’re caused by a sudden, covered event. And even then, it’s not guaranteed.

What Counts as a Foundation Leak?

A foundation leak isn’t just a wet spot on the floor. It’s water intrusion that compromises the structural integrity of your home’s base. This can show up as:

- Cracks wider than 1/8 inch in basement walls or slabs

- Water seepage after heavy rain or snowmelt

- Musty odors or mold growth near the foundation

- Uneven floors or sticking doors that didn’t exist before

These aren’t just cosmetic issues. Left unchecked, they can lead to shifting soil, wall bowing, or even structural collapse. But insurance companies don’t treat them like fire or lightning damage. They look at the root cause.

When Insurance Might Cover It

Your homeowners insurance could pay for foundation repairs if the leak resulted from a sudden and accidental event listed in your policy. These are the only scenarios with a decent chance of approval:

- A burst pipe inside the wall that flooded the basement

- Water damage from a broken water heater or washing machine overflow

- Damage from a fallen tree hitting the house and cracking the foundation

- Fire or explosion that caused structural damage

In these cases, the foundation damage is treated as a secondary effect of a covered peril. For example, if a pipe bursts and water floods your basement, the insurer will cover the cost to fix the pipe, dry out the area, and repair any cracked foundation caused by the water pressure. But if the pipe burst because it was old and corroded? That’s maintenance-and you’re on the hook.

What’s Almost Always Excluded

Most foundation leaks are caused by slow, gradual processes that insurers classify as wear and tear or poor maintenance. These are almost never covered:

- Hydrostatic pressure from groundwater buildup over time

- Shifting soil due to drought, clay expansion, or poor drainage

- Settling of the foundation over years (normal for homes 10+ years old)

- Cracks from poor initial construction or substandard materials

- Leaky gutters or downspouts that directed water toward the foundation for months

These are considered preventable. Insurance isn’t meant to replace regular upkeep. If your home has a history of minor leaks that you ignored, don’t expect coverage when the problem escalates. Insurers have teams that review claims for signs of long-term neglect. A photo of water stains from five years ago? That’s a red flag.

What About Flood Insurance?

People often confuse foundation leaks with flood damage. If your basement fills up because of a nearby river overflowing or heavy rainfall overwhelming city drains, that’s a flood-and standard homeowners insurance won’t touch it. You need a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private provider. But even then, flood insurance usually only covers damage from external water sources, not internal plumbing failures or groundwater pressure under your slab.

And here’s the catch: if your leak is caused by groundwater rising due to saturated soil, and you live in a flood zone, insurers may still deny your claim, arguing it’s a flood event-even if the water came from under your house, not from outside.

How to Prove It’s Covered

If you believe your foundation leak qualifies for coverage, you need documentation. Insurance adjusters don’t take your word for it. They want:

- Photos and videos of the damage taken immediately after the event

- Records of recent weather events (heavy rain, freezing temps, etc.)

- A licensed contractor’s report identifying the cause

- Proof that the damage was sudden-not gradual

For example, if a pipe burst on January 15 and your basement flooded, take photos the same day. Call a plumber to locate the leak. Get a written statement from them saying the pipe failed due to age and pressure, not corrosion from neglect. Then hire a structural engineer to confirm the foundation crack was caused by the floodwater, not pre-existing settling. Without these, your claim will likely be denied.

What to Do If Your Claim Is Denied

Denials are common. In fact, over 60% of foundation-related claims are rejected in the first round, according to data from the Insurance Information Institute. But you can appeal.

Start by requesting a written explanation of the denial. Look for keywords like "gradual damage," "wear and tear," or "excluded peril." Then get a second opinion from an independent structural engineer. Sometimes, the adjuster misclassified the cause. If the second report says the damage was caused by a sudden freeze-thaw cycle that cracked a sewer line-which then leaked into the foundation-you have a fighting chance.

You can also ask your insurance agent to escalate the claim. Some companies have special review teams for contested claims. And if you’re still stuck, your state’s insurance commissioner’s office can mediate disputes.

Prevention Is Cheaper Than Repairs

The best way to avoid a denied claim? Prevent the leak before it starts. Here’s what actually works:

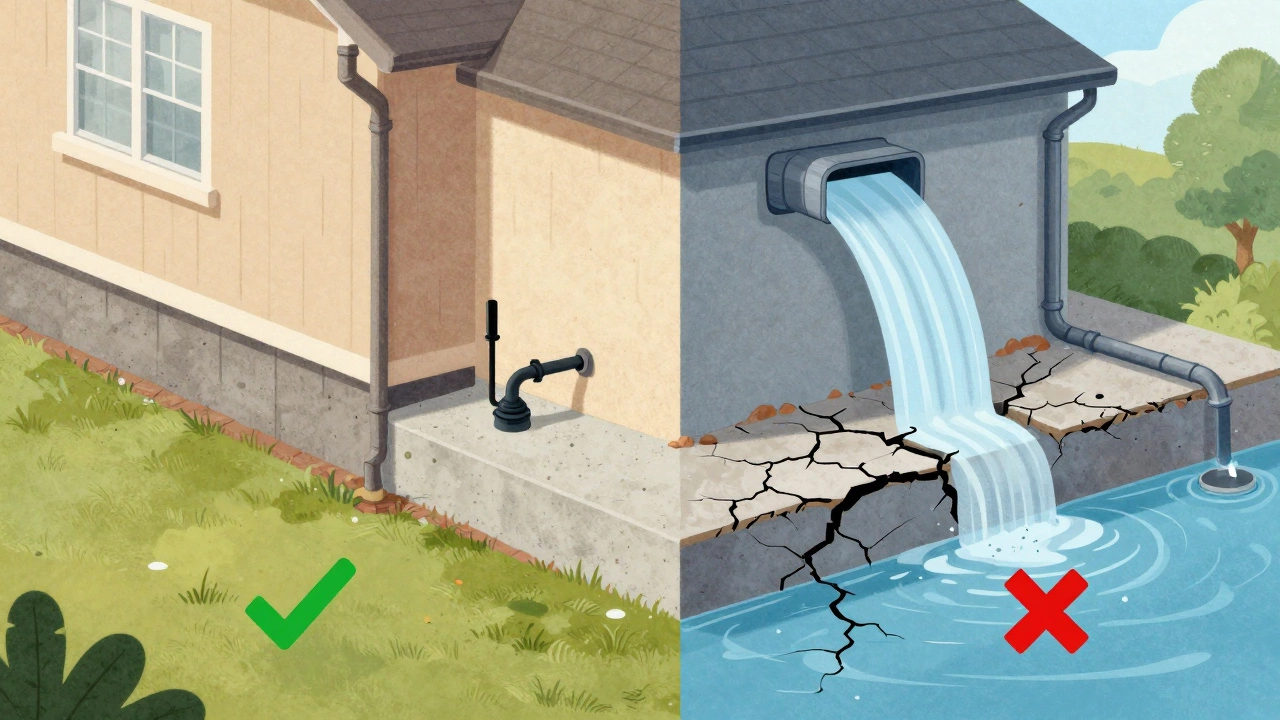

- Keep gutters clean and extend downspouts at least 6 feet from the foundation

- Grade soil away from your home so water flows outward, not inward

- Install a sump pump with battery backup in basements prone to moisture

- Seal cracks in concrete with hydraulic cement every 2-3 years

- Check for plumbing leaks behind walls and under sinks at least twice a year

These steps cost less than $500 total and can prevent hundreds of thousands in damage. And if you do it consistently, you’re more likely to get approved if something unexpected happens.

Special Considerations for Older Homes

If your house was built before 1980, your foundation is likely made of unreinforced masonry or poured concrete without proper drainage. These older foundations are more vulnerable to water damage. Insurance companies know this. Some even offer limited coverage for older homes-but only if you can prove you’ve maintained the property. Keep receipts for:

- Foundation sealing

- Drainage system installations

- Plumbing upgrades

- Soil grading work

Having a paper trail of maintenance can be the difference between a denied claim and a paid one.

When to Call a Foundation Specialist

If you see any of these signs, don’t wait:

- Cracks wider than a credit card

- Stair-step cracks in brick or block walls

- Doors that won’t close properly

- Visible gaps between the foundation and the siding

Call a licensed foundation repair company. They’ll do a free inspection and give you a report. That report can help your insurance claim-if the damage is recent and caused by a covered event. But if the inspector says the damage has been developing for years? You’ll need to pay out of pocket.

Does homeowners insurance cover foundation cracks?

It depends on why the cracks happened. If they were caused by a sudden covered event-like a tree falling on your house or a burst pipe flooding the basement-then yes, repairs may be covered. But if the cracks are from settling, soil shifting, or long-term water exposure, they’re considered maintenance issues and won’t be covered.

Can I get coverage for foundation leaks if I add a rider?

Most standard policies don’t offer riders for foundation leaks caused by groundwater or soil movement. Some insurers offer "water backup" coverage, which helps if a sump pump fails or a sewer line backs up into your basement. But this won’t cover cracks from external water pressure. You’ll need to pay for preventive measures yourself.

Is foundation repair covered if I have a home warranty?

Home warranties typically cover mechanical systems like HVAC, plumbing, and electrical-but not structural elements like foundations. Even if your warranty covers a leaking pipe, it won’t pay to fix the cracked concrete it damaged. You’ll need insurance or out-of-pocket funds for that.

How much does foundation repair usually cost?

Costs vary widely. Minor repairs like sealing cracks cost $300-$800. Major fixes like underpinning or slab jacking range from $5,000 to $15,000. If the entire foundation needs replacement, you’re looking at $20,000-$40,000. Insurance rarely covers these costs unless the damage was sudden and caused by a covered peril.

Should I get flood insurance if I live on a hill?

Even if you’re on higher ground, heavy rain can still cause groundwater pressure to build under your foundation. Flood insurance won’t cover this type of leak, but if your area has experienced flash flooding in the past-even once-it’s worth considering. Flood maps change, and what was "low risk" five years ago might now be moderate. Check your local flood zone map.

Final Thoughts

Your homeowners insurance is designed to protect you from disasters-not neglect. Foundation leaks are rarely a surprise. They develop slowly. Water seeps in over months. Cracks widen with each freeze-thaw cycle. If you’ve ignored the signs, don’t be shocked when the insurer says "no." But if you’ve stayed on top of maintenance and something sudden happens-a pipe bursts, a storm knocks over a tree-then you’ve done everything right. That’s when insurance works the way it’s supposed to.

The bottom line: Know your policy. Document everything. Act fast. And if you’re unsure, call your agent before the next rainstorm hits.